Dividend stocks are the Swiss army knives of the stock market.

When dividend stocks go up, you make money. When they don’t go up — you still make money (from the dividend). Heck, even when a dividend stock goes down in price, it’s not all bad news, because the dividend yield (the absolute dividend amount, divided by the stock price) gets richer the more the stock falls in price.

Knowing all this, wouldn’t you like to find great dividend stocks? Of course you would.

Wall Street analysts have chimed in – and they are recommending two high-yield dividend stocks for investors looking to find protection for their portfolio. These are stocks with a specific set of clear attributes: a dividend yield of at least 8% and Strong Buy ratings. Let’s take a closer look.

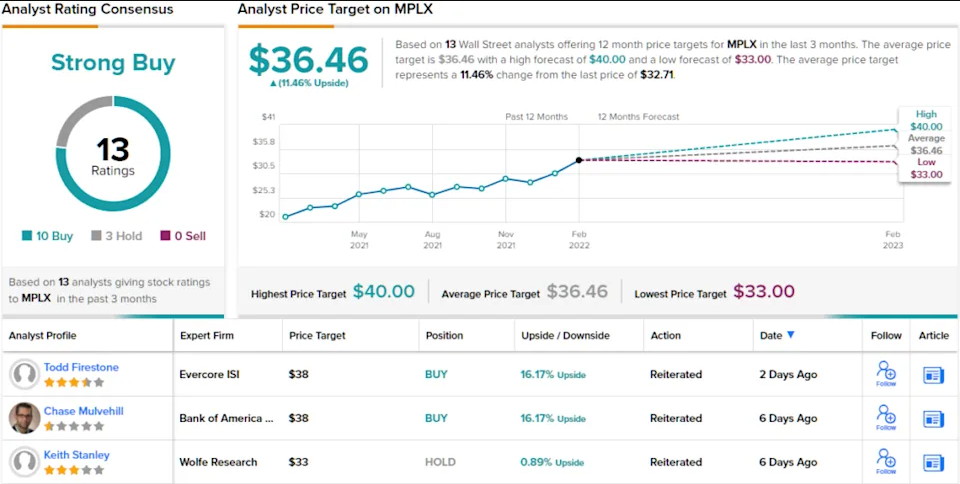

MPLX LP

We’ll start in the energy industry, where MPLX operates a diverse range of oil and gas infrastructure assets, including pipelines, river shipping, terminals, refineries, and storage facilities. The company’s asset network extends from Washington State to the Rocky Mountains, and from the Gulf Coast to the Great Lakes.

While the Biden Administration has taken a decidedly anti-fossil fuel stance, and especially an anti-pipeline stance, MPLX shares are up 55% in the past 12 months. The stock has benefited from rising oil and gas prices, and consequent higher prices for fossil fuel transport and storage.

The company’s income has been rising for the past several quarters, and in 4Q21 MPLX reported 78 cents per share in earnings. This was 4% higher than the 75-cent forecast. At the top line, revenue came in at $2.73 billion, up from $2.25 billion in 4Q20.

In addition to solid top and bottom line, MPLX generated $1.2 billion in distributable cash flow, and raised the common share dividend to 70.5 cents. At that rate, the dividend annualizes to $2.82 per common share and gives an impressive yield of 8.6%.

Looking forward, RBC analyst TJ Schultz sees MPLX as a company in a sound position to keep bringing returns to shareholders. He writes: “MPLX beat Street estimates on solid commodity-based G&P margins resulting from the strong NGL price environment. MPLX continued distributing meaningful capital to unitholders through unit repurchases and distribution. MPLX provided 2022 capex guidance which is expected to be allocated toward expansion and optimization projects of existing assets in preparation for expected higher producer activity.”

In line with these comments, Schultz rates MPLX an Outperform (i.e. Buy), and his $40 price target implies it has room for 22% growth going forward. Based on the current dividend yield and the expected price appreciation, the stock has ~31% potential total return profile.

Overall, this fundamentally sound energy company gets a Strong Buy rating from Wall Street’s analyst consensus, based on 13 reviews that include 10 Buys against 3 Holds. The shares are selling for $32.71 and the $36.46 average price target indicates ~11% upside potential from that level.

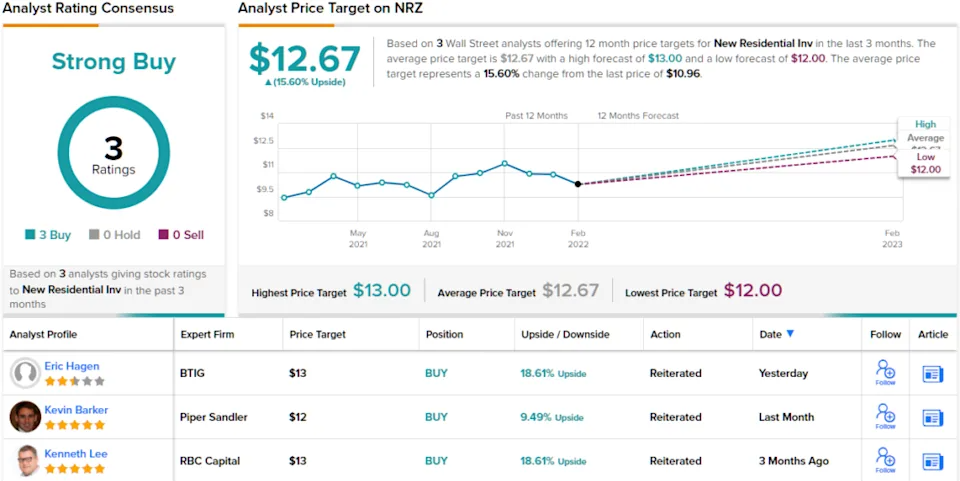

New Residential Investment (NRZ)

Now let’s shift gears, from energy to real estate. New Residential is a Real Estate Investment Trust (REIT), a class of companies that are among the market’s best dividend payers. New Residential holds a portfolio worth approximately $6 billion, with nearly two-thirds of that total invested in mortgage origination and mortgage servicing.

The company reported 4Q21 results on February 8, before the market opening – and a look at the numbers may be enlightening. In that quarter, the company saw earnings of 40 cents per share, down 11% from the previous quarter but up 25% year-over-year. Core earnings came to $191.9 million, and the company had $1.33 billion in cash assets available.

The liquid assets and cash are a key point, as they fund the dividend. In December, New Residential declared a payment of 25 cents per common share, or $1 annualized, which was paid out at the end of January. At that rate, the dividend yields 9.8%, a rate far higher than the average dividend found among companies listed in the S&P index, and while bonds are starting to rise, New Residential’s dividend still yields an impressive 5x the 10-year Treasury bond’s rate.

BTIG analyst Eric Hagen points out the upcoming change in the Fed’s interest rate policy may increase risk in the mortgage sector, but lays out a case for NRZ regardless, saying, “We like staying long. The risk of higher funding costs remains the primary sensitivity point on forward earnings, although that feels largely incorporated into the valuation at 0.85-0.90x NAV. We also see some earnings upside from continuing to unlock cost synergies…”

Hagen’s comments come along with a Buy rating on the stock, while his price target of $13 suggests that New Residential has an upside of 27% ahead of it this year.

Hagen is not the only analyst on Wall Street who likes this REIT; New Resi has picked up 3 reviews recently and they are all positive, for a unanimous Strong Buy consensus rating. The shares are selling for $10.20 while the average price target is $12.67, indicating a one-year upside of 24% for 2022.

Hagen’s comments come along with a Buy rating on the stock, while his price target of $13 suggests that NRZ has an upside of ~19% ahead of it this year.

Hagen is not the only analyst on Wall Street who likes this REIT; New Resi has picked up 3 reviews recently and they are all positive, for a unanimous Strong Buy consensus rating. The shares are selling for $10.96 while the average price target is $12.67, indicating a one-year upside of ~16% for 2022.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.